Know Your After-Tax Return: If you're in the accumulation phase of life and live in a high-tax state like California, New York, or New Jersey, it’s worth being intentional about where you hold different types of investments.

One of the biggest mistakes I see investors make is owning income-generating assets in taxable accounts without understanding the after-tax impact. These investments often kick off ordinary income which, for many high earners, means getting taxed at rates north of 45%.

Just because something earns 7% on paper doesn't mean you're actually keeping 7%.

This isn't a piece about the investment merits or portfolio benefits/downsides of private credit, REITs, or covered call strategies. However, before you allocate to them, you need to ask one simple question:

What’s the true after-tax return?

If you have access to tax-deferred or tax-free accounts (IRA, 401k, Roth, etc.), that’s often a better place for these strategies.

Here are a few common investments I’d think twice about owning in a taxable account:

Again, context matters. Your financial goals, income level, and tax bracket all play a role in what’s best for your situation. This isn't specific advice, but rather a framework for asking the right questions.

To make this a bit more real, lets use a live example.

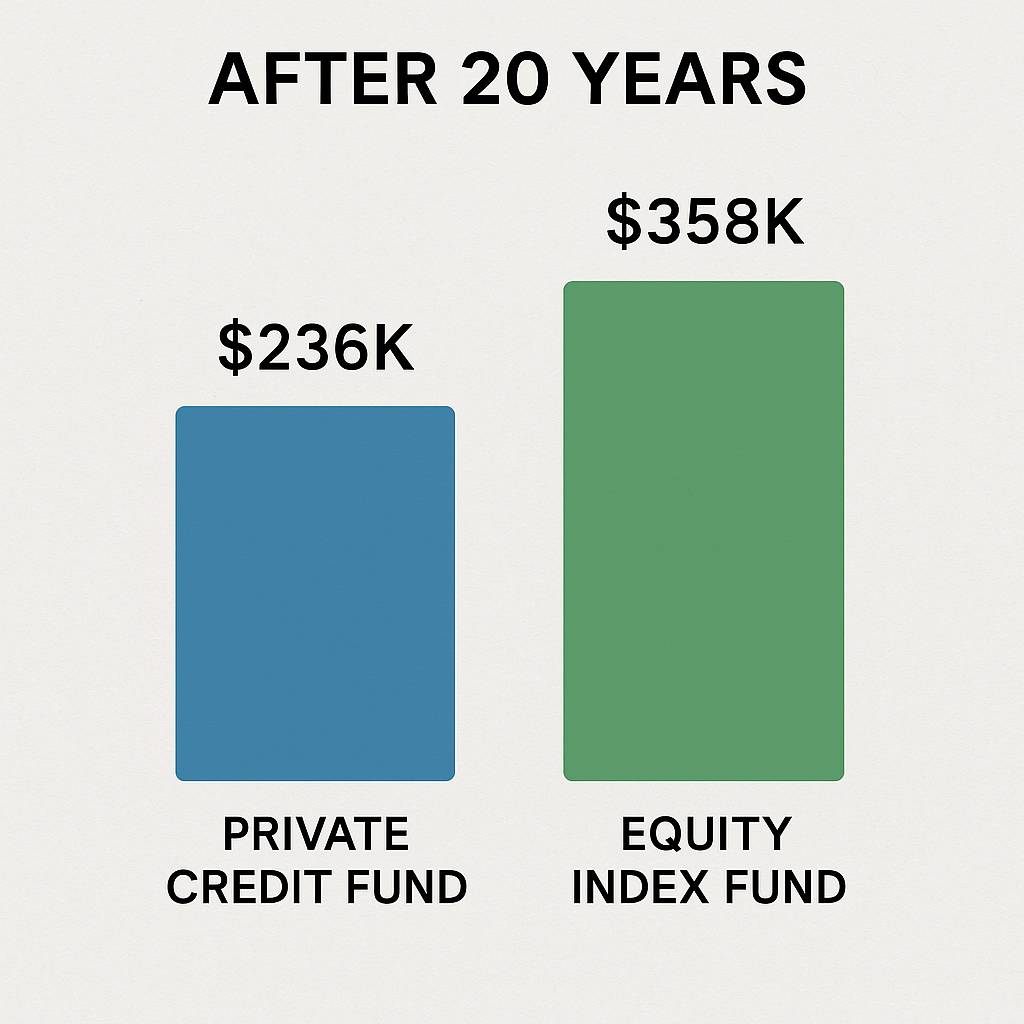

Let’s assume you invest $100,000 into two different vehicles, each earning 8% annually for 20 years:

After 20 years:

Even with the same headline return, the structure and tax treatment of an investment can create a massive difference over 20 years.

Tax drag is real and it matters more than most people think.

Buy Once, Cry Once: I’m not Dave Ramsey. I'm not a budgeting specialist. Because of this, I rarely write about spending habits. It feels personal. However, I want to break my rule today because this isn't really about spending.

I recently stumbled across a philosophy that’s stuck with me: Buy Once, Cry Once.

The idea is pretty simple. It’s better to feel the pain of paying for a quality item once than to deal with the ongoing annoyance (and hidden cost) of replacing something cheap multiple times. It's not just about things either. It's about services too.

As a society, I feel like we fall into the trap of buying what is “good enough.” Fast fashion does this to us. Shoes that wear out in six months. Kitchen tools that break under pressure. Even software platforms or service providers that looked cheaper on the surface but end up costing time, stress, or both.

I'm slowly realizing that it's just not worth it.

I recently discovered the Saddleback Leather brand, whose tagline says it all: “They’ll fight over it when you’re dead.” Yes, their bags are expensive. But they’re meant to last a lifetime. They offer a 100 year warranty. That kind of durability in both products and businesses has become something I deeply value.

Don't get me wrong, this isn’t just about buying nice things for the sake of it. It’s about intentionally choosing fewer, better things. Choose to partner with businesses (or people) who prioritize quality above all. I admire anyone who takes the long view. Whether it’s a craftsman building a leather bag to last 100 years, or a founder choosing to scale slowly so they can deliver excellence, not just speed.

There’s a hidden upside to all of this too. When you start prioritizing quality, you start needing less. Life becomes simpler. Better. More durable.

What other brands fit this mold?

Stompy the Bear:

I swore I wouldn’t be that parent. I wouldn't blast toddler music in the car like it’s the latest Drake album. But here I am. My son now throws out song requests like a mini DJ every time we get in the car.

And I’ll admit it. Stompy the Bear slaps.

It’s got this weird jam vibe that just works. The beat is catchy, the chorus is chaotic in the best way, and somehow, we both end up head-banging by verse two.

I still try to sneak in my Spotify playlists from time to time, but I'm content listening to my son's requests. Stompy the Bear rises to the top.

Parenthood has humbled me in many ways. This is just one more tally on the scoreboard.

Disclaimer: VDB Wealth is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed. Past performance is not indicative of future performance.

We work with a select group of clients to provide tailored, high-touch wealth management. Ready to see how we can help?

Our personalized process ensures you receive expert financial guidance tailored to your unique goals. Get in touch in the way that works best for you—fill out the contact form, send us an email, or schedule a call. However you choose to reach out, we’re here to help you build, grow, and protect your wealth.

VDB Wealth LLC is a registered investment adviser located in the State of Georgia. Registration as an investment adviser does not imply a certain level of skill or training.

The information on this website is for informational purposes only and does not constitute investment, legal, tax, or financial advice. Nothing on this site should be interpreted as a solicitation, offer, or recommendation to buy or sell any securities or investment products. All investments involve risks, including the potential loss of principal.

VDB Wealth LLC provides investment advisory services only to residents of states where it is properly registered or exempt from registration. Past performance is not a guarantee of future results.

VDB Wealth LLC | (415) 209-5862 | contact@vdbwealth.com